How to make the most of your money using neon

Money has come a long way since its invention: The development from metal-based currencies to paper money and eventually to electronic transactions, credit cards, and online banking took thousands of years. All the while, one thing didn’t change: People always wondered how to best manage their hard-earned money.

If you also wonder how to best use the various solutions neon offers to manage your money, you’ve come to the right place. In this blog article, we’re going to look at different strategies of money management: From holding your money in your Main Account to the riskier but potentially rewarding investments in stocks and ETFs, it's crucial to grasp the intricacies of each option. That’s why, in this comprehensive guide, we'll explore the various trade-offs, all while considering risk, return, and liquidity. And to top it off, we're not only visualising everything in handy graphs that look like spiderwebs, but we're explaining everything with analogies from Spiderman. Let's have some fun!

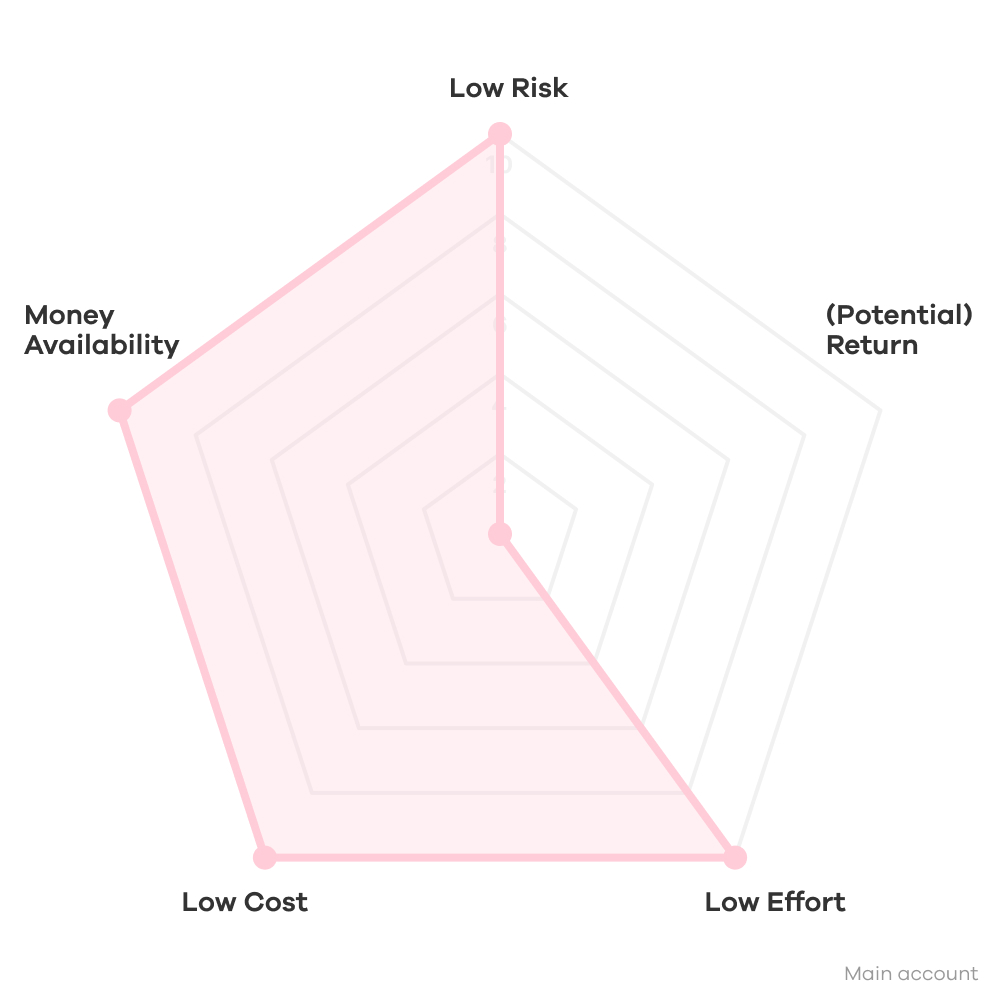

Keeping your savings in your neon Main Account − aka with great power comes great responsibility

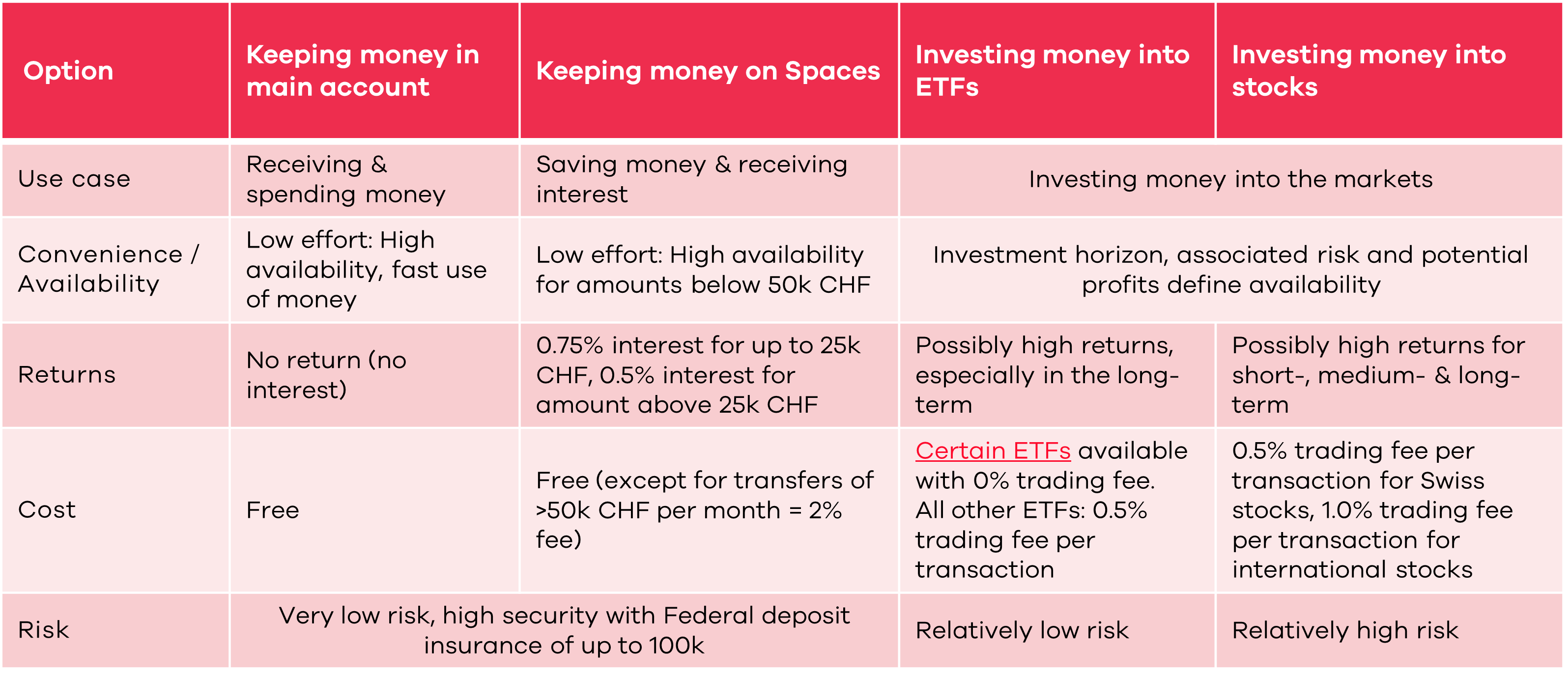

Keeping your money in your Main Account on neon is definitely the better option than keeping cash under your mattress at home. Not only because deposits of up to 100’000 CHF in your neon account are insured by the Federal Government’s deposit insurance, but also because the money in your Main Account is easily accessible and you can spend it when, where, and how you want.

However, since you don’t receive any interest for deposits on your Main Account, inflation will eventually eat away at your purchasing power, meaning that with a 0% interest rate, the real value of your savings in the Main Account will decrease over time, especially in periods of high inflation.

Translated to Spider-Man’s world: When Peter Parker wanted to impress Mary Jane by buying a car, he competed in a wrestling match and won thanks to his spidey skills. But he was eventually cheated out of his prize. Then, out of revenge, Spidey didn’t help the venue owner when he got robbed, and later that very robber killed Spider-Man’s uncle. So, the moral of the story is: If Spider-Man doesn't act, evil takes over (as much as inflation takes over your money when you don't act). Therefore, remember: With great power comes great responsibility, which means the willingness to act (on your money) in the first place. Otherwise, by keeping money in your Main Account, you have no real opportunity for wealth accumulation, making it less favourable for achieving long-term financial goals.

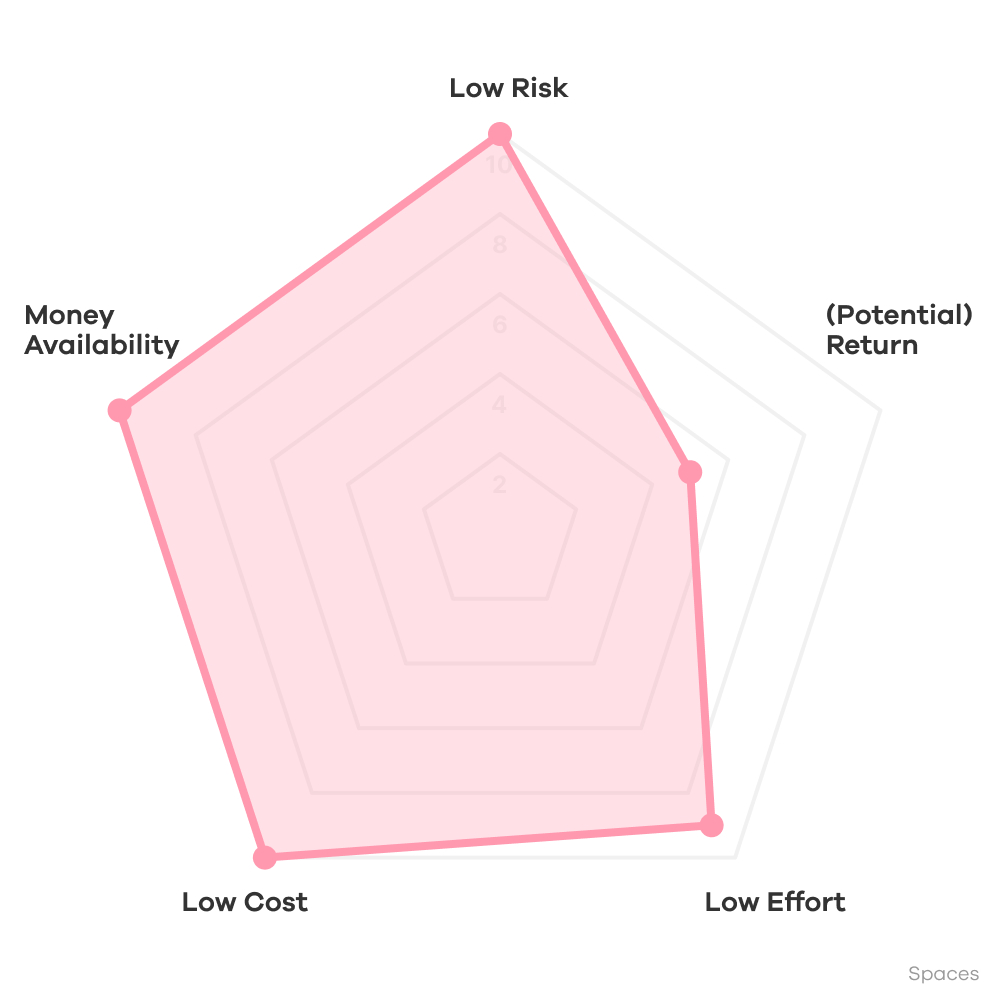

Earning up to 0.50% interest for keeping your savings on neon Spaces − aka saving Mary Jane

Opting to shift your savings from your Main Account to your Spaces gives you an advantage of 0.50% (or 0.25% for deposits exceeding 25’000 CHF) thanks to the interest on Spaces. The interest you earn on neon Spaces provides an increase in the value of your savings over time (however, only as long as you earn enough interest to beat inflation). Meanwhile, you have very low risk because your money is safe and you can access it easily and quickly: When you need to use some of your money you parked on your Spaces, you can simply shift it back to your Main Account and use it within a maximum of 30 minutes (= high liquidity). This makes neon Spaces the perfect place to put the money you need as a safety net for unforeseen events and short-term projects.

Let’s translate to tingle your spidey senses: Putting money on your Spaces is like Spider-Man saving Mary Jane from criminals. What you gain from it (the interest aka the rewarding kiss and general love interest from MJ) is pretty good when you compare it to the effort and risk involved – transferring your money to your Spaces is as easy-peasy as it is for the mighty Spider-Man to fight off some petty criminals in the streets.

Back to the real, non-Marvel world: Note that there is a cumulated limit of 50'000 CHF per calendar month in place on withdrawals from Spaces to your Main Account. If you exceed this limit, you will have to pay a 2% fee at the end of the year on the exceeding amount. Hence, if you plan to withdraw more than 50'000 CHF in one month, you can split your withdrawals between the end of one month and the beginning of the next, since the limit applies to a full calendar month.

Now, let’s have a look at the – comparatively small – disadvantage of keeping your savings in your Spaces: Opportunity cost. Simply put, if you were to use the money you keep in your Spaces for another strategy, you could generate higher returns than the 0.50/0.25% you get as interest on Spaces. Let’s translate again: If Spider-Man did not save MJ, he would have the opportunity to save another girl and potentially get a higher reward than MJ’s kiss (we leave it up to you to what that might be). But that involves a lot of «ifs and buts» along with other unknown factors, meaning higher risks. Let’s have a look at two of those possible strategies with higher potential returns next.

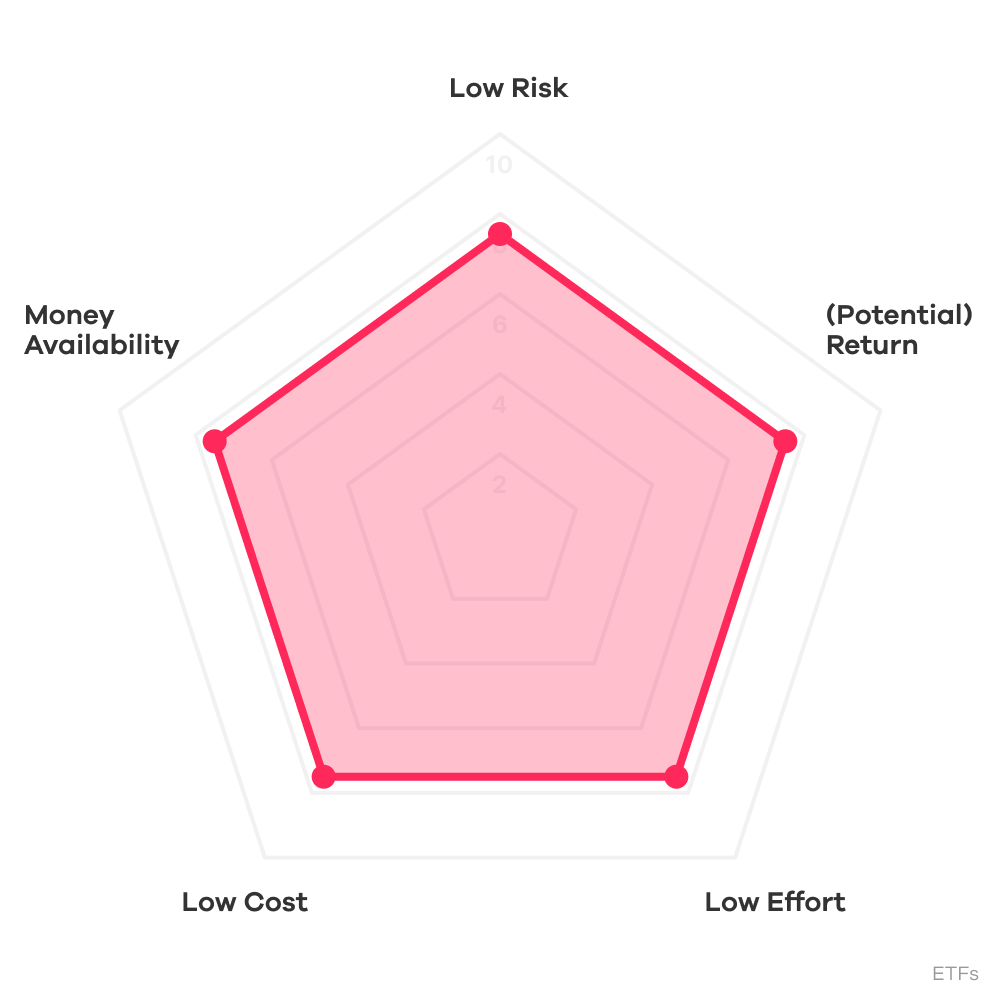

Investing your savings into ETFs with neon invest − aka saving MJ and the gondola

First off, if you don’t know what ETFs are, have a look at this blog article. Done? All right, now you know that ETFs combine the diversification benefits of mutual funds with the tradability of stocks, while also typically moving up and down less heavily (= lower volatility) than the prices of certain stocks. You also know that with ETFs, you can invest your savings across a broad range of assets (= diversification), which reduces – but never completely eliminates – risk. That’s why it makes a lot of sense to buy and hold ETFs for the long term – and even more so with neon invest, since there are no custody account fees. Equipped with this knowledge, what would you do if you were Spider-Man and the Green Goblin gave you the choice of saving either Mary Jane or a gondola full of people? You'd split (diversify) your power, save them both and laugh at the fact that the Green Goblin doesn't know anything about diversification... er sorry, of your powers. You'd laugh at his lack of understanding of your powers.

While you manage to save both MJ and the gondola full of people (in your portfolio), it is by no means a risk-free task. The same holds true for ETFs: While they are usually less risky than single stocks, they still hold some risks, since they are subject to broader market movements − despite their diversification. You can buy and sell ETFs throughout the trading day on your neon app and therefore have your money quickly available if you need it (= liquidity). However, this liquidity is also linked to risk. Because if the price of your ETF drops and you need your invested money right there and then, you might see yourself forced to sell at a loss. Now that you know the most important things about ETFs, feel free to browse the selection of ETFs available on neon invest, where you can buy and sell ETFs with a low trading fee of 0.5% per transaction – or for no trading fee at all with certain ETFs on neon invest.

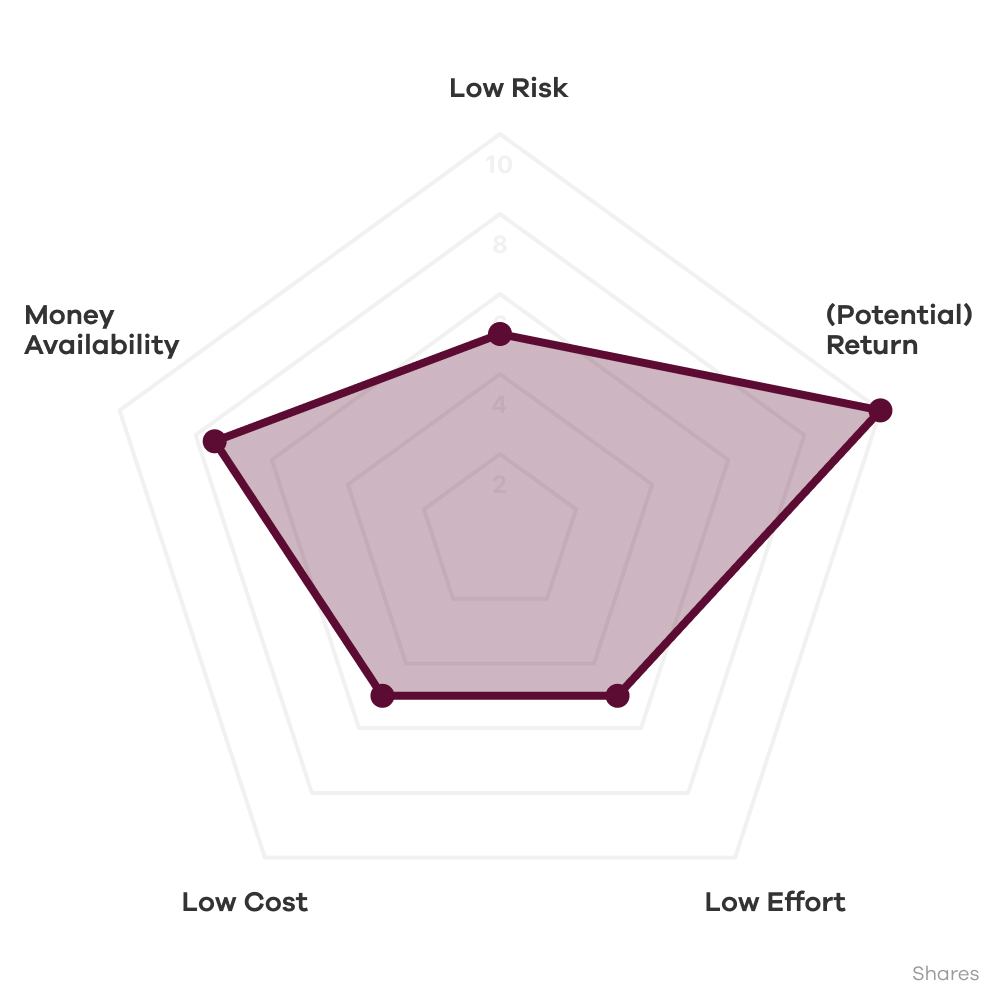

Investing your savings into shares with neon invest − aka winning against the Green Goblin

In the real world, the main advantage of investing in stocks of innovative companies that are thriving and expanding economically lies in the prospect of high returns, especially if you intend to hold your investments for the long term. But also here, investing comes with a certain risk. In the Marvel universe, the same holds true: If you invest in bringing down a green individual, the gain is big − the world becomes a better place −, but the risk − evil takes over or you could even lose your life − is considerable.

Successful (!) stock investments can significantly outpace inflation by generating high returns. But generally speaking, the higher the potential returns are, the higher the risks are as well – and the high level of risk is also the main disadvantage of investing your money in stocks. Because factors over which you have no control, such as market volatility (aka New York’s support of Spider-Man), company-specific risks (aka the Green Goblin’s strength and weaknesses), and economic conditions (will Aunt May let Spider-Man stay forever?) can lead to significant losses. So, if your risk tolerance is low, investing in single stocks is probably not the most suitable solution for you. In other words: If your risk tolerance is low, you probably shouldn’t be Spider-Man.

If you intend to hold your investments for an extended period, having a portfolio with neon invest is especially worth it because there are no custody account fees. Also, buying stocks via neon invest comes at a very low cost of 0.5% per transaction for Swiss shares and 1.0% per transaction for international shares.

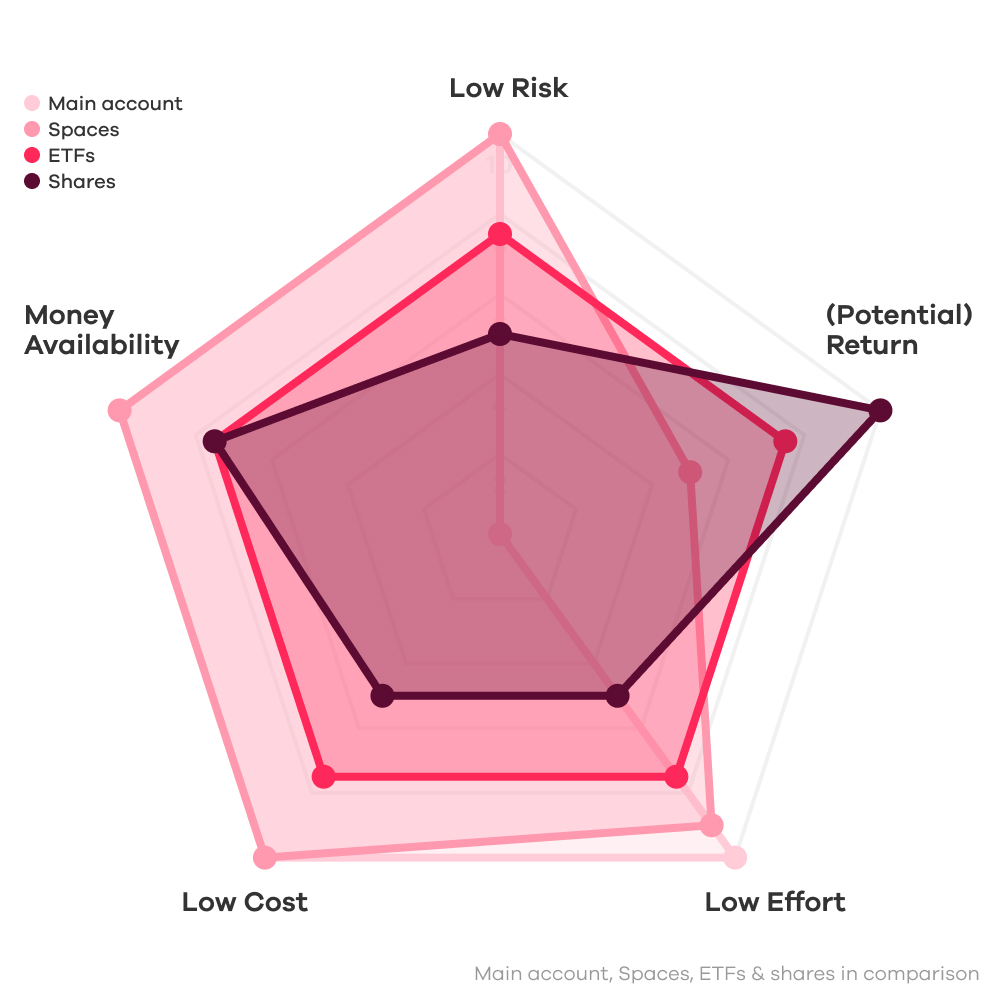

In conclusion, the choice of what to do with your savings should be based on your individual financial goals, your personal risk tolerance, and your investment horizon (i.e., how long you can afford to keep your savings invested). While Spaces offer security and liquidity, they might not generate enough returns to keep inflation from eating away at your money. On the other hand, investing in stocks or ETFs can potentially generate higher returns but comes with varying levels of risk. It is essential to diversify one's portfolio and conduct thorough research or seek professional advice before making any investment decisions. Balancing risk and return is key to achieving financial stability and growth over the long term. To finish things off, here is a handy overview table of what you’ve just read, as well as one single spider graph displaying all the options for better comparison:

Please read this before using neon invest! 👇

This blog article is an advertisement in accordance with Art. 3. lit. g FIDLEG. Its aim is to inform you about neon invest. Nevertheless, it does neither constitute a recommendation to buy or sell any specific financial instruments nor does it serve as financial or investment advice. In other words:

It is up to you if you use neon invest or not.

Therefore, we suggest you seek guidance from independent experts (which we're obviously not) before you engage in neon invest. Always remember that investing involves inherent risks and that it's crucial to only invest money that you can afford to lose – in the worst case all of it. And finally, you should know that past performance of financial instruments never predicts the future. If you want to read the complete version of this disclaimer in proper legalese, please head this way.