Demystifying Swiss mortgages with neon

Are you considering purchasing your first «Home Sweet Home» in Switzerland?

For this, you most probably will need a mortgage, and we know that the Swiss mortgage market might seem like a maze at first. That’s why, in this article, we want to demystify the jargon and break down the most important things you need to know.

You don’t need expert knowledge at all to read this article: We’ll take you by the hand and explain it in simple terms. And if you need a quick refresher before we take off, you can click on the following links to see the definition of: a mortgage and interest rates.

In Switzerland, you (almost) never fully own your house

Renting vs. owning: What's best for me?

Fixed vs. variable interest rate

How do I pay back my mortgage?

What is the rental value or Eigenmietwert?

What factors determine whether or not I am granted a mortgage?

Why do my friends get different interest rates for a similar house?

What is the key to get the best interest rate?

In a nutshell – a few tips for your mortgage

First, in Switzerland, you (almost) never fully own your house

Wait, what? Well, this is probably the first thing that you need to know to really understand the Swiss home financing mechanics: You usually just own one third of the property and keep a mortgage on the other two thirds of the property value. You can practically renew your mortgage indefinitely, and even pass it on to the next generation, so that they, too, can save on taxes.

Taxes? Indeed, most of the costs associated with paying off a mortgage, such as maintenance costs or interest-rate payments, are deductible in the tax return. This tax optimisation gives you a strong advantage when purchasing your home with a mortgage.

You never have to reimburse the total amount of your mortgage. Instead, you only have to pay back a part of it. That’s also why you sometimes hear that Swiss financial institutions own most of the property market. And that’s true!

Still, also just partly owning your house can be very interesting in order to save on costs such as taxes compared to other situations like renting. Here’s why:

Renting vs. owning: What’s best for me?

You are wondering if you should take out a mortgage to purchase a house instead of renting your house?

First, you need to know that owning a house in Switzerland is not necessarily much cheaper than renting one, there is a cut-off interest rate where it makes more sense to buy or rather rent. That’s why you need to understand how the market works and be aware of your overall financial situation.

As a homeowner, your costs are: The interest of the loan, the amortisation cost (the part of the house’s value that is requested to be reimbursed by the financial institution), the maintenance costs, and the tax relating to the rental value («Eigenmietwert») – even if you don’t rent your house (we’ll explain this specificity of the Swiss market further below).

As a renter, your costs are: The rent, plus your 3a since when you chose to have one (though this is independent from your rent, of course).

To find out if owning makes more sense for you than renting, you need to assess your costs as an owner and compare them to your costs as a renter, and project them into the future.

| Cost type | Owner | Renter | Comments |

| Rent | ✖️ | ✔️ | Your monthy rent |

| Rental value («Eigenmietwert») |

✔️ | ✖️ |

Fictional rental income from your property, will be added to your taxable income |

| Interest rate payments |

✔️ | ✖️ | Price for lending the mortgage, tax deductible |

| Amortisation | ✔️ | ✖️ |

Payments to pay back the requested part of your mortgage, could be via pilar 3a |

| Pilar 3a | (✔️) | (✔️) |

Optional but recommended for owners and renters, owners can use the pilar 3a payments for an (indirect) amortisation,it is tax deductible. |

| Maintenance costs | ✔️ | ✖️ |

Costs to maintain your property, note: value-preserving investments are tax deductible |

To assess your individual situation, you can reach out to mortgage experts. Later in this article, we will introduce one of our partners that can support you when it comes to mortgages: MoneyPark. Read on to find out more.

As you can see, you should be pragmatic and dot your i’s and cross your t’s before deciding to buy your dream property. Once you’ve checked all the boxes, you can get the keys and pop the Champagne.

Choose your strategy: Fixed vs. variable interest rate

When it comes to mortgages, you can choose between two interest rate types: Fixed-rate mortgages or variable-rate mortgages. Or you combine them in several mortgage tranches.

A fixed-rate mortgage is a type of mortgage where your interest rate constantly remains on the level of when you take out a mortgage. Your interest rate remains the same throughout the entire term of your mortgage contract.

For example, if your aunt Sofia offers you to purchase her flat in the suburb of a city and you take out a fixed-rate mortgage at, let’s say, 2.5% interest rate, the interest rate will stay at 2.5% regardless of any changes in the broader interest-rate environment. Fixed-rate mortgages provide you with predictability and stability for your monthly mortgage payments, making it easier to budget for the long term.

Variable-rate mortgages are types of mortgages where your interest rate can change during the term of your mortgage contract.

The most famous type of variable-rate mortgages is the SARON mortgage. It can change daily based on the prevailing market conditions. SARON stands for «Swiss Average Rate OverNight» and is a reference rate that represents the interest rate at which Swiss banks lend money to each other on the money market. If the SARON rate goes up, your mortgage rate goes up, and if it goes down, your mortgage rate goes down accordingly. Therefore, this type of mortgage can provide lower initial interest rates, making it especially attractive for borrowers to choose mortgages with a short duration in a low interest environment. However, it also exposes borrowers to market fluctuations and therefore to interest rate risk, as the payments can fluctuate based on changes in the Swap rate.

Choosing between fixed or variable rates depends on your risk tolerance, financial stability, mortgage duration, and on your outlook on and knowledge of the financial market. There’s no one-size-fits-all answer, that’s why it’s a good idea to seek advice from experts in the field before making this decision.

For example, you can reach out to our partner MoneyPark. They provide impartial advice by comparing the mortgage offers of more than 150 financial institutions across Switzerland.

Now, let’s get back to the basics of the mortgage market:

What is equity?

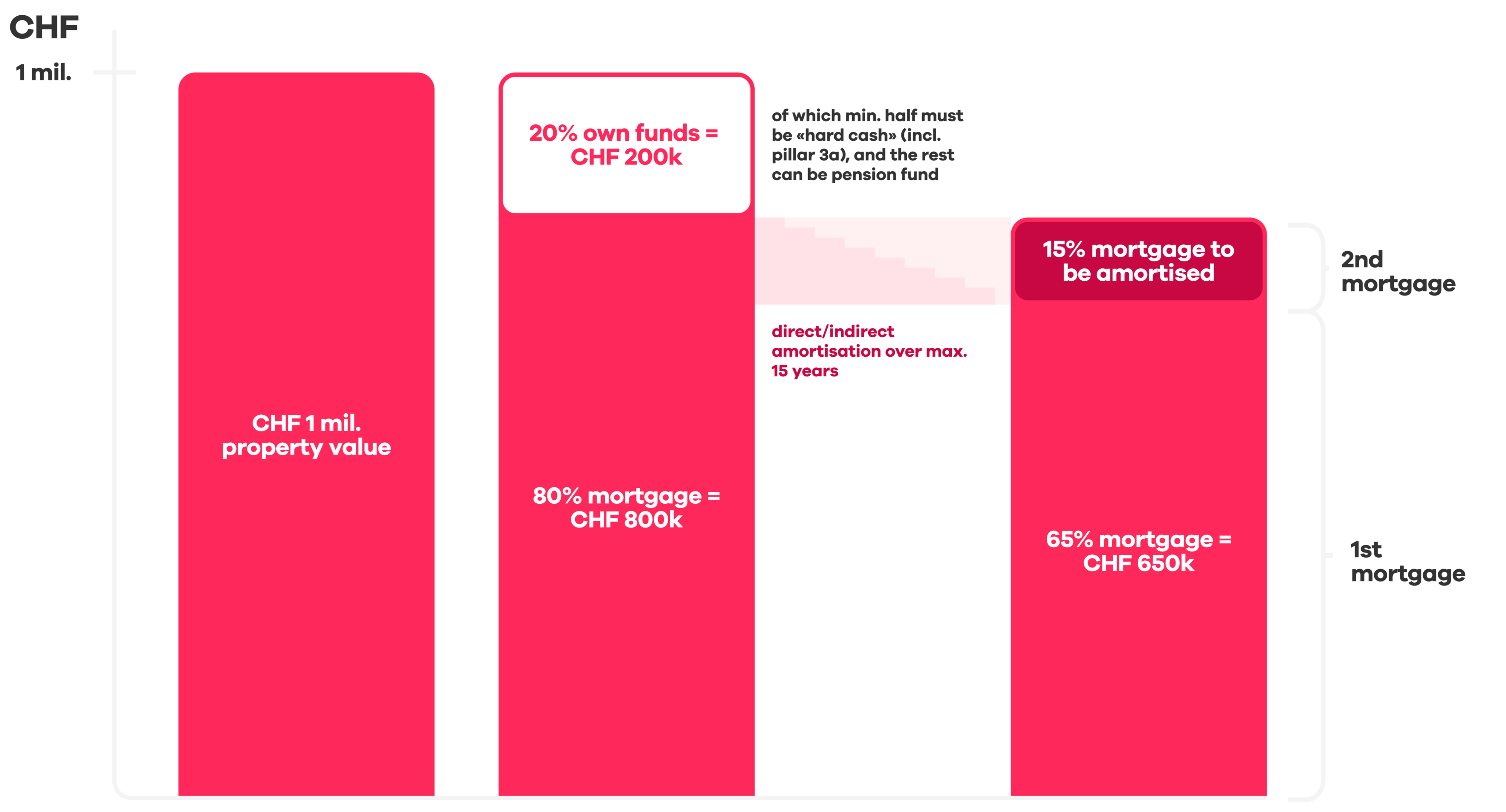

Equity is the initial investment required for a property purchase (also referred to as «own funds»). In Switzerland, the rule is to have at least 20% of the property value in own funds. This means that if your aunt Sofia offers you to purchase her flat for 1 million CHF, you should have (at least) 200’000 CHF of equity to inject into the purchase. At least, because other costs of buying are associated with your purchase. Half of your equity has to be “hard cash”, for the rest you can draw from various sources to meet the equity requirements: For example from your savings, by pledging your pension fund or your pillar 3a, or by using an advance inheritance.

If you want to assess if you have enough equity for purchasing your dream home, you can do so using this handy calculator developed by MoneyPark. And if you want to understand if it’s more interesting to withdraw or to pledge your pension fund assets – yes, both are possible and can be interesting depending on your situation – you can find more details in this article (in German).

What is the LTV ratio?

The Loan-To-Value (LTV) ratio represents the share of the money you borrow in the property’s value. In Switzerland, either the market value of the property or its purchase price, whichever is lower, determines the property value as collateral («Niederstwertprinzip») against a loan, also called «collateral value».

The LTV is calculated based on this collateral value. In the example of your aunt Sofia’s flat, if your equity for this property purchase is 200’000 CHF and the apartment’s collateral value is 1’000’000 CHF, your loan would be 800’000 CHF, and your LTV ratio is 80%.

Often, 80% is the maximum LTV, and if half of your equity is composed by your pledged pension fund, you get a 90% «gross-LTV».

Graph: relation between property value and its financing via own funds, mortgage, and amortisation). Note: For reasons of presentation 65% and 15% were used instead of 66.67% and 13.33%.

On the contrary, an LTV below 66.67% is considered to be on the lower side of risk. In some cases, when the LTV ratio is high, you might want to consider taking out a mortgage insurance or a pillar 3a product from an insurance company in order to improve your LTV. Because the LTV directly influences the overall terms of your mortgage, it’s a key consideration in the mortgage process, helping both borrowers and lenders to assess the risk associated with the loan.

There are a couple of other things to consider regarding mortgages. For example, you might wonder how to pay back a mortgage and what factors determine whether or not you are granted a mortgage. You might also wonder why the interest rates are different depending on the provider offering it or why your interest rate differs from the one your friends get. Let’s clarify!

How do I pay back my mortgage?

As a reminder, a specificity of the Swiss mortgage market is that you almost never have to pay back your mortgage entirely. If you missed that part, take another look at this blog post’s first paragraph.

The whole process of repaying the loan is called «amortisation». And the part that financial institutions in Switzerland will ask you to pay back is called the «second mortgage», while the part that will remain (in most cases) and enable tax deductions is called the «first mortgage». Together, your first and second mortgage consist of up to 80% of the property’s value (that is, your LTV).

For the amortisation, financial institutions will ask you to pay off parts of the loan so that your LTV is not higher than 66.67%. If your LTV is above 66.67%, you are still in the second mortgage.

Of course, you can amortise (reimburse) more of the first mortgage, but this does not always make sense in terms of taxes.

The amortisation schedule cannot exceed 15 years if you are between 18 and 50 years old. If you’re above 50, you can amortise your mortgage until you retire (usually at 65 years old).

Repayments must follow a pattern: A set amount has to be paid at regular intervals, e.g. monthly or quarterly.

What is the rental value or «Eigenmietwert»?

The «Eigenmietwert» is another specificity to the Swiss mortgage market. It could be described as a fictional rental income from your property.

This income must be taxed, even if you do not rent out the house but live in it yourself. Basically, the tax authorities add the rental value to your taxable income. Unfortunately, there is no unique formula to calculate the rental value for your property.

This is why it’s interesting to keep a first mortgage ongoing after amortising the second mortgage: Thanks to the renewed mortgage, you can deduct the mortgage’s interest, its amortisation, and the (value-preserving) house maintenance costs from your taxes. This should ideally cover for the additional taxes you got from the Eigenmietwert, plus tap into some of your usual revenue taxes.

The Eigenmietwert’s calculation follows the canton’s rules in which the property is located. So you always need to make a projection of your current salary’s taxes and the Eigenmietwert you would get. You then subtract the interest, amortisation and maintenance costs to see how much you could save on your taxes thanks to your first mortgage.

What factors determine whether or not I am granted a mortgage?

The main factor for this is your affordability. It is comparing your income against your liabilities connected to your property in the space of one year. Your affordability also includes a 5% threshold for interest rates (in case of an unexpected increase), called «calculatory interest rate», meaning that you need to be able to afford it even if the overall market conditions turn worse, i.e. mortgage interest rates go up to 5%. Your liabilities include your recurring expenses, your amortisation payments, and your mortgage’s interest rates. Your affordability is also called your expense-to-income ratio.

To be eligible for a mortgage in Switzerland, for most lenders, the total annual expenses associated with the mortgage shouldn’t add up to more than one third (33%) of your income. But as mentioned above, its calculation varies. Each lender also decides if and how your savings, pensions, and additional income will be considered as income when calculating your affordability. Note: A second income (for instance, from your spouse) should only be added to the equation if your home is mortgaged in exchange for a joint home loan.

Why do my friends get different interest rates for a similar house?

First, because your equity (how much of your own money you’re investing) and your affordability (financial capacity to pay back the loan) are probably not the same as your friends’ – this influences the rates you get.

But besides this, it’s important that you understand that the Swiss mortgage market is not just about interest rates and the property’s value.

To know if taking out a mortgage is worth it for you, and to make the right decision at each step, you need to take a holistic approach of your overall financial situation, including your taxes, life and invalidity insurances, direct or indirect amortisation, and tax-deductions.

What is the key to get the best interest rate?

The key for getting the best interest rate is to compare different mortgage providers and negotiate offers. Ask various financial institutions – banks, insurance companies, pension funds.

You can do so by asking our partner MoneyPark to compare the mortgage offers of over 150 providers in Switzerland.

By comparing different offers tailored to your specific situation, you’ll soon find out that the best offer is not always the one you expect.

In a nutshell – a few tips for your mortgage:

Before we call it a day, let’s summarise the top advice to follow in your mortgage hunt:

1. Know and understand your financial situation.

2. Use online calculators to assess your affordability and your LTV.

3. If your LTV is high, talk to a professional advisor about drawing from your pension assets to lower it.

4. Find your dream property matching your financial situation.

5. Last, but not least: Think twice before splitting your mortgage into tranches, as it might tie you with the same financial institution in case of renegotiations – and in less favourable terms.

You can find more detailed steps in this blog article from Baloise.

You have further questions on mortgages, for instance you’d like to better understand the last point above and find out if you’d be tied to the financial institution from which you borrow? Or you want to learn more about mortgage renegotiations in general? We’ve got you covered: Simply click here to read our dedicated blog article.

Remember: Even if we try to lighten up the Swiss mortgage landscape for you in this blog, it will always remain a blend of options, risks, and rewards. But by seeking professional advice, you’ll be fully equipped to navigate this landscape and secure the mortgage that sets you on a path to successful property ownership.

Happy nesting!

NB: With our partnership with MoneyPark, we also earn some money. Just like with all our partners.

Quick refresher-Appendix

What is a mortgage?

A mortgage is a type of credit that you can take out to purchase or maintain a home, land, or other types of real estate. As a borrower, you agree to pay the lender (a bank, or another financial institution such as a pension fund or insurance) over time, typically in a series of regular payments, the «amortisation». And the property then serves as collateral to secure the loan.

Now, there are other important things to understand about mortgages: Interest rates.

What are interest rates?

Interest rates are the cost of borrowing money from a lender. It is usually expressed as a percentage of the total amount borrowed. When you take out a mortgage, you’re essentially borrowing money from a lender to buy a property. The interest rate is the additional amount you pay on top of the amount you borrowed (and will be reimbursing over time) as compensation to the lender for allowing you to use their money. Like for any loan.

If you want to get back to the first paragraph of this blog article, click here.