Bank fees part 1: general information

Lots of factors play a role when choosing a bank. But for most of us, price is key. As part of this, we look at the basic fees charged for the account and the card, and we might look at the fees for cash withdrawals, too – but we rarely devote much attention to the details otherwise.

However, that’s exactly where you can get caught out. Of course, what your bank account will actually cost, and what’s the best choice for you, depends on what you do with your money. Are you someone who’s always travelling, or making purchases abroad (including on Amazon and the like)? Or do you prefer to use cash and are constantly popping to the ATM as a result?

An independent platform like moneyland.ch can help you compare what’s out there. Think about which user profile is most like you and what you’re expecting.

As moneyland.ch has investigated, Wise and Revolut might be among the cheapest card providers, but they’re not covered by the Swiss deposit protection scheme. And without a Swiss IBAN, they’re far from the ideal account for your salary to be paid into or for making payments within Switzerland. Since January 2020, neon has also been offering the interbank rate overseas – just like Revolut – and we’re even covered by the Swiss deposit protection scheme. So, are we practically unbeatable? For a normal bank account used for making payments and purchases both in Switzerland and overseas, many banks would charge you fees of at least 150 CHF a year, with some larger banks even coming in at 200 CHF.

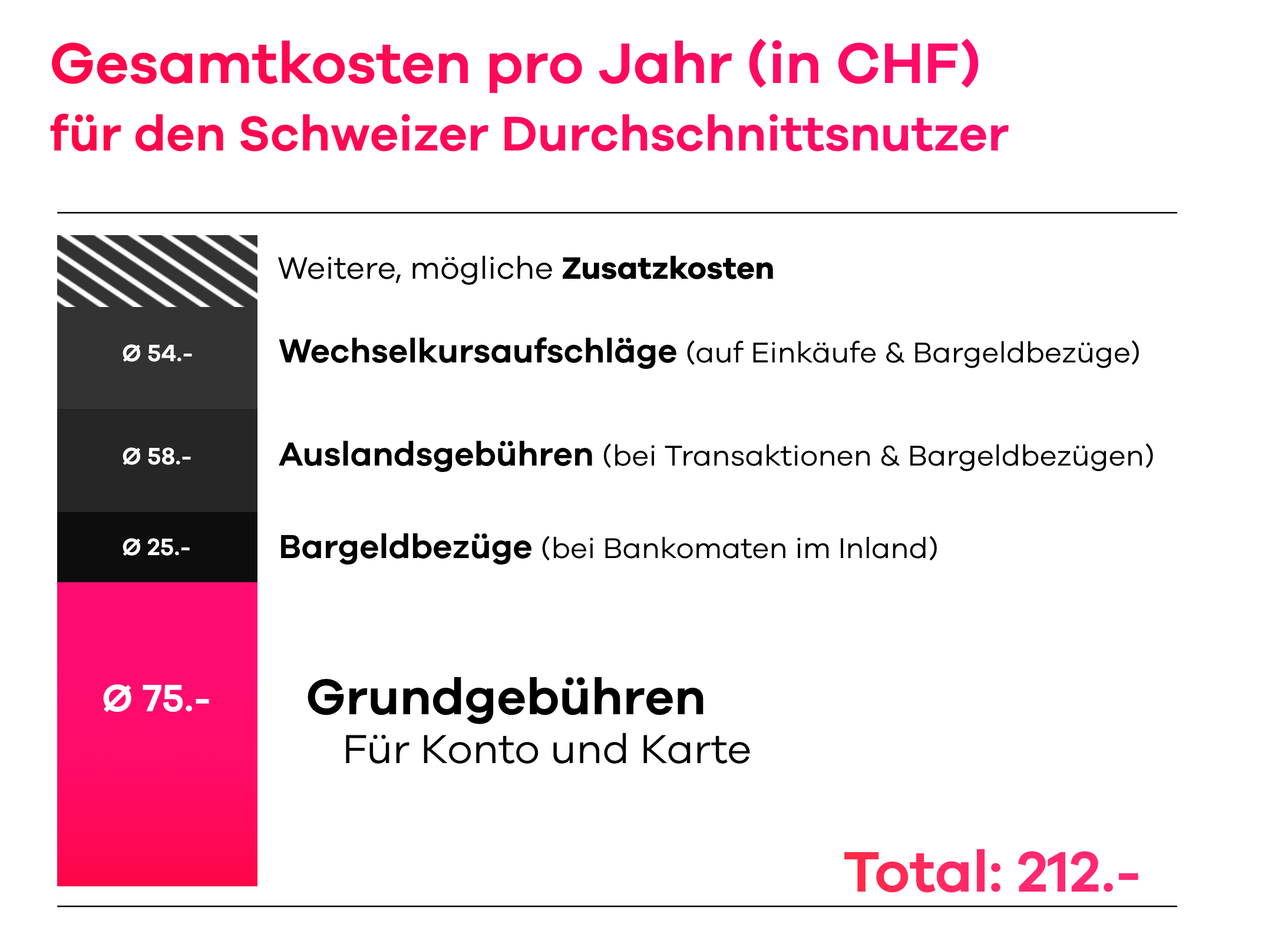

But how do these fees tot up to 200 CHF so easily? It’s helpful to break this down. Roughly speaking, bank fees can be divided into various categories: there are basic fees (for your account and your card) and cash withdrawal fees, plus overseas fees and the currency conversion surcharge. Many also charge additional fees for specific services, such as if you lose your card or a bank statement.

Translation:

total costs per year (in CHF)

for the average Swiss user

-other, possible additional costs (on purchases & cash withdrawals)

-foreign fees (for transactions & cash withdrawals)

-cash withdrawals (at domestic ATMs)

Basic fees for account and card

All the data is taken from moneyland.ch (25 September 2018). The data corresponds to the average Swiss user, born 1991, online banking only. A comparison was made between the top 8 banks in terms of pricing: Freiburger KB, Appenzeller KB, UBS, CS, PostFinance, St. Galler KB, Luzerner KB, Cler, Hypothekarbank Lenzburg. The average of the 8 banks was used to depict the costs.

Basic fees

This category includes the basic fees for your account and card(s). Lots of banks try to attract customers by charging zero basic fees for apprentices or students during their first year, but if you stick with your bank for a few years, this first free year is of no consequence. Others tout their free accounts, but their extra fees add up to well in excess of 100 CHF.

Cash withdrawals

Generally speaking, withdrawing money from your own bank is free. If you want to make a withdrawal from a different bank, you’ll easily pay 2 CHF to 5 CHF per withdrawal. And that quickly adds up, especially if your bank doesn’t have a big network of ATMs. So, it’s worth thinking about how often you need to take out cash, and where and when you do it.

Additional costs

Sure, nobody plans to lose their card once a year. That said, it’s still worth taking a look at these costs. If you lose your card, you’ll often have to pay for a replacement, and for blocking the old card, too – and a figure of 70 CHF isn’t unheard of.

Spend lots of time abroad or love online shopping? Read part 2 here

Now you’re wondering: what’s the situation with neon? And what makes neon so appealing?