Bank fees part 2: overseas fees

In this part, we’ll explore what happens when you spend money abroad. Incidentally, this also includes online payments on Amazon, eBay, etc., which often incur overseas usage fees and currency conversion surcharges.

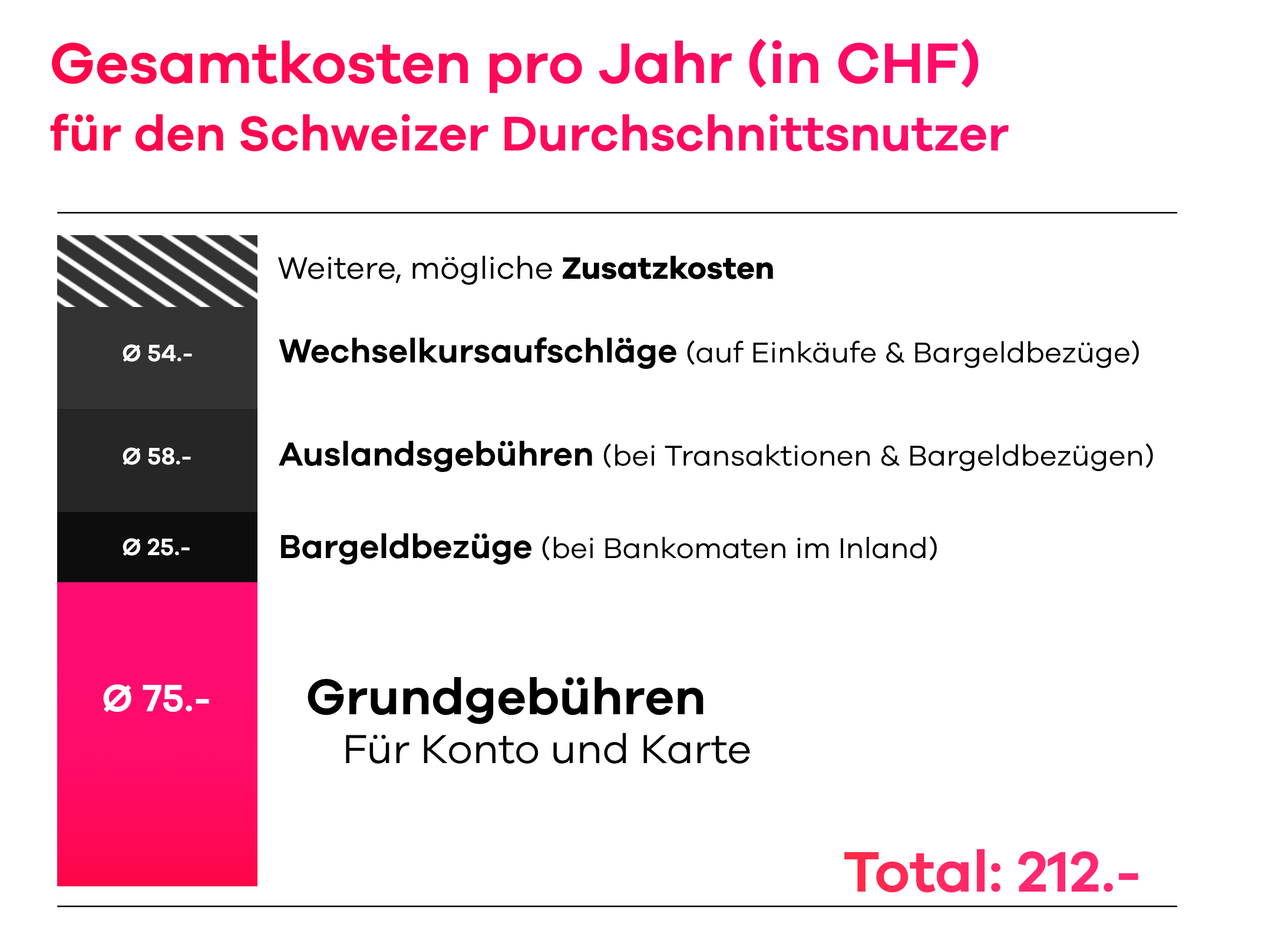

Translation:

total costs per year (in CHF)

for the average Swiss user

-other, possible additional costs (on purchases & cash withdrawals)

-foreign fees (for transactions & cash withdrawals)

-cash withdrawals (at domestic ATMs)

Basic fees for account and card

All the data is taken from moneyland.ch (25 September 2018). The data corresponds to the average Swiss user, born 1991, online banking only. A comparison was made between the top 8 banks in terms of pricing: Freiburger KB, Appenzeller KB, UBS, CS, PostFinance, St. Galler KB, Luzerner KB, Cler, Hypothekarbank Lenzburg. The average of the 8 banks was used to depict the costs.

Overseas usage fees

Overseas usage fees can be divided into two categories: fees for cash withdrawals and fees for transactions. Both of these types can be either a percentage or a set amount, and there are normally different figures for Maestro cards and credit cards. In terms of taking out cash, you’ll usually pay a fixed amount for each withdrawal, such as 5 CHF. Withdrawals are often cheaper with your Maestro card than your credit card. In other words, it generally makes sense to use your Maestro card for taking out cash.

You’re often charged a percentage when you make a payment with your credit card in a shop or online, typically set at between 1.5% and 3% of the amount in question. Conversely, the fees incurred by your Maestro card are often fixed amounts, such as 1.50 CHF per transaction. That makes it hard to compare the two. Generally speaking, it’s cheaper to use your credit card for smaller sums and your Maestro for bigger sums. However, Maestro is often not accepted outside Europe.

Currency conversion surcharge

The currency conversion surcharge is by far and away the hardest fee to understand because it’s not a transparent charge. In other words, it’s not identified directly. When currencies are converted, banks can access an interbank rate that’s much lower than the exchange rate you’ll get to see. The following example illustrates how it works when you buy a bag overseas for 100 EUR.

Source: neon. Icon credits: price tag icon made by Gregor Cesnar from www.flaticon.com Bag: free vector design by: https://www.vecteezy.com/vector-art/91460-vector-bags-icons (only German version available)

At the end of the day, you’ll pay 120 CHF for your purchase of 100 EUR. Your bank earns 7 CHF, a surcharge of 6.2% on the actual value of the goods.

It’s often hard to find out what your bank’s currency conversion surcharge is. Some banks declare it in a footnote within their detailed price lists, whereas others stress that you can call their customer service team and they’ll tell you. However, you can also calculate your bank’s currency conversion surcharge yourself. Every day, the interbank rate is listed on websites like oanda.com, for example. Check it out and compare this exchange rate with what your bank charges you.

Now you’re wondering: what’s the situation with neon? And what makes neon so appealing?

Missed part one? There, we explore basic fees, cash withdrawals and more